✅Scenario 1

Moderate tightening (common case)

- Driver exits spread over time

- Most rule components hold

- Demand grows slowly

Spot impact: steady upward pressure with lane spikes.

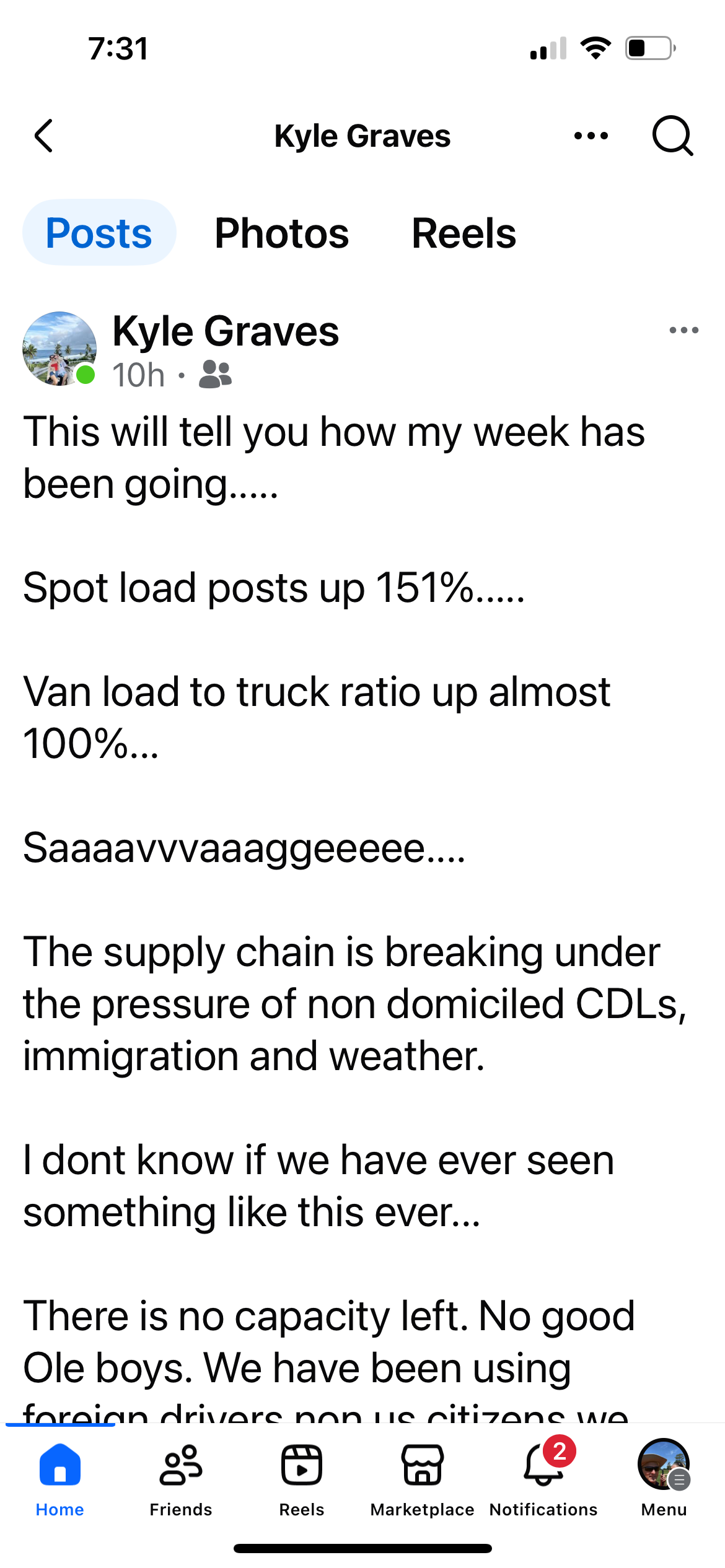

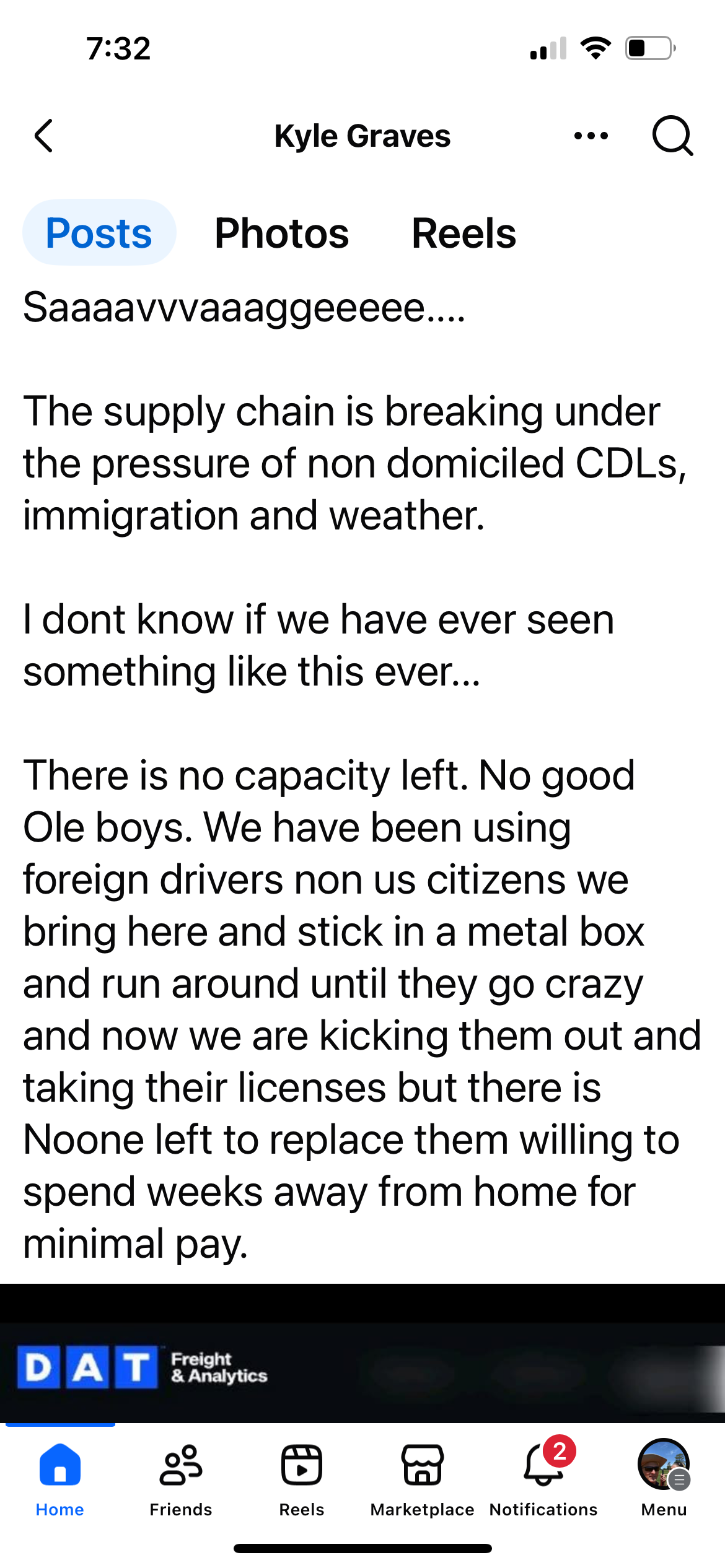

FMCSA’s non-domiciled CDL rule is reshaping the U.S. driver pool. As licenses get harder to obtain and renew, capacity tightens — and the truckload spot market reacts first.

In this guide, we unpack what the rule actually changes, how driver supply could shift, and how those changes may pressure truckload spot rates across van, reefer, flatbed, and power-only through 2026.

A non-domiciled commercial driver’s license (CDL) is a CDL issued to a driver who is legally present and authorized to work, but who does not meet a state’s traditional definition of being “domiciled” as a permanent resident.

In practice, a non-domiciled CDL holder often:

When rules tighten around a meaningful subset of working drivers, the ripple effect shows up in driver supply, capacity, and ultimately price per mile — especially in the spot market.

FMCSA’s direction is to tighten eligibility and verification so CDL issuance is backed by clearer documentation and consistent processes across states. On the ground, this introduces friction into a labor pool many fleets rely on.

In practical terms, the rule can drive changes like:

Because the issue overlaps transportation safety, state licensing, and immigration policy, it’s also become a legal and political flashpoint. Enforcement may vary by state and timing, but the long-term direction is tighter verification.

Timing may shift with legal outcomes, but if renewals tighten, driver supply tightens — and the spot market responds first.

Estimates vary, but the key point is scale: even a gradual exit of tens of thousands of active drivers can move capacity in specific lanes. Exits won’t happen overnight — they follow renewal cycles and enforcement timelines.

If fleets compete harder for fewer qualified drivers, wages and recruiting costs rise. That increases a carrier’s break-even point and supports higher pricing over time.

Capacity tightening won’t feel uniform. Expect sharper pressure where non-domiciled driver concentration is higher and where freight is already tough to cover.

If driver supply tightens while demand holds, the market has fewer safe, compliant trucks available — and spot pricing tends to move higher first.

The simplest way to think about 2026 is that this rule can act as a capacity “floor” — reducing the amount of slack in the system. That increases the odds of sharper spot spikes during seasonal surges and disruptions (weather, produce, retail swings).

Without policy pressure, many forecasts would assume gradual tightening. With driver supply friction layered in, spot can rise faster than contract, especially in lanes where coverage is already thin.

| Equipment Type | Baseline Outlook | Policy-Adjusted Outlook |

|---|---|---|

| Dry Van | Modest growth | Higher volatility; sharper lane spikes |

| Reefer | Seasonal swings | More aggressive peaks in produce/retail cycles |

| Flatbed / Step-Deck | Cyclical | Upward pressure in active regions if demand holds |

| Power-Only | Stable | Upward pressure where repositioning relies on tight labor pools |

Because timing and enforcement can change, scenarios are the most honest way to plan.

Spot impact: steady upward pressure with lane spikes.

Spot impact: sharper volatility and stronger peaks.

Spot impact: uneven, lane-dependent movement.

Need help running lanes for net profit? See our truck dispatch services.

It can support higher spot pricing by tightening driver supply, but the size depends on enforcement timing and the broader economy.

Lanes and segments with thinner coverage and higher non-domiciled driver concentration often feel tightening sooner.

Yes. If volumes fall materially, capacity tightening may absorb excess trucks instead of driving large rate jumps.

Strong dispatch helps you: